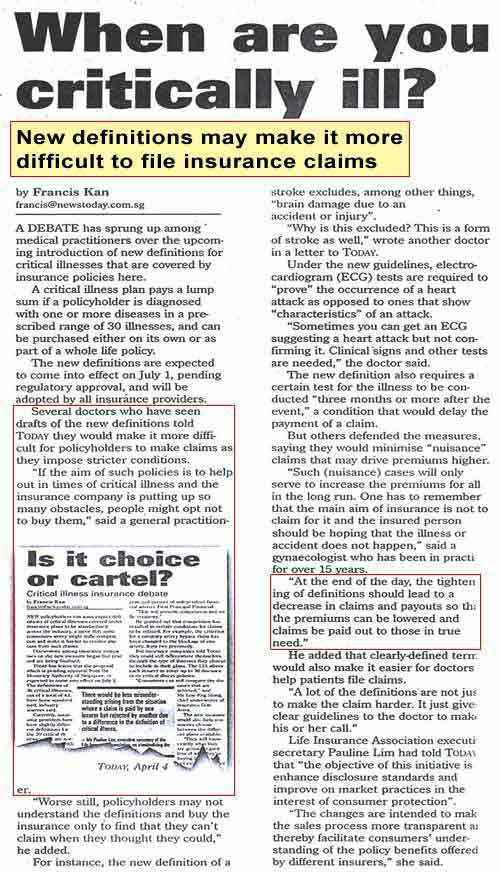

Current Critical Illness Definition

1. Heart Attack

The death of a portion of the heart muscle as a result

of inadequate blood supply to the relevant area. The following features

must be present: a) A history of typical chest pain b) New ECG changes

characteristic of myocardial infarction c) Elevation of cardiac enzymes

2. Stroke

Any cerebrovascular incident producing neurological sequelae

lasting more than twenty-four hours and including infarction of brain

tissue, heamorrhage and embolisation from an ex-cranial source. There

must be evidence of permanent neurological deficit.

3. Coronary Artery Disease (Surgery)

The undergoing of heart surgery to correct narrowing or

blockage of one or more coronary arteries with bypass grafts in persons

with limiting anginal symptoms, but excluding non-surgical techniques

such as balloon angioplasty or laser relief of an obstruction.

4. Cancer

A malignant tumour characterized by the uncontrolled growth

and spread of malignant cells and the invasion of tissue. This includes

leukaemia, but excludes non-invasive cancer in situ, tumours in the

presence of any human immuno-deficiency virus and any skin cancer other

than malignant melanoma.

5. Kidney Failure

End stage renal disease, due to whatever cause(s), w the

life assured undergoing regular peritoneal dialysis or haemodialysis

or having had renal transplantation.

6. Paralysis

Complete and permanent loss of use of two or more limbs

through paralysis.

7. Major Organ Transplantation

The actual undergoing as a recipient of a transplant of

a heart, lung, liver, pancreas, kidney or bone marrow.

8. Multiple Sclerosis

Unequivocal diagnosis by a consultant neurologist confirming

more than one episode of well defined neurological deficit, w persisting

signs or involvement of e optic nerves, brain stem and spinal cord together

w impairment of co-ordination and motor and sensory function, w e life

assured not necessarily confined to wheelchair.

9. Fulminant Viral Hepatitis

This involves a submassive to massive necrosis of the

liver caused by the Fulminant hepatitis virus leading precipitously

to liver failure as certified by a registered medical practitioner.

The diagnostic criteria to be met are: a) A rapidly decreasing liver

size b) Necrosis involving entire lobules, leaving only a collapsed

reticular framework c) Rapidly degenerating liver function tests d)

Deepening jaundice. The illness must not be caused directly or indirectly

by drug abuse.

10. Pulmonary Arterial Hypertension

Primary pulmonary arterial hypertension as established

by clinical and laboratory investigations (including cardiac catheterization)

and as diagnosed by a consultant cardiologist. The following diagnostic

criteria must be met:

11. Blindness

Total and irrecoverable loss of sight in both eyes.

12. Alzheimer's Disease

Deterioration or loss of intellectual capacity or abnormal

behaviour as evidenced by the clinical state and accepted standardized

questionnaires or tests arising from Alzheimer's Disease or irreversible

organic degenerative disorders (excluding neurosis and psychiatric illness)

resulting in significant reduction in mental and social functioning

requiring the continuous supervision of the life assured.

13. Surgery to the Aorta

Surgery to correct any narrowing, dissection or aneurysm

of the thoracic or abdominal aorta.

14. Coma

A state of unconsciousness with no reaction to external

stimuli or internal needs persisting continuously with the use of life

support system for a period of at least 96 hours and resulting in permanent

neurological deficit.

15. Deafness

Total and irreversible loss of hearing in both ears.

16. Loss of Speech

Total and irrecoverable loss of ability to speak due to

physical damage to the vocal chords.

17. Heart Valve Surgery

Open heart surgery to correct valvular abnormalities

18. Major Burns

Third degree burns covering at least 20 percent of the

surface area of the life assured's body.

19. Terminal Illness

In the opinion of the medical specialist involved and

subject to the acceptance of our appointed doctor the advent of death

is highly likely within 12 months.

20. AIDS

* AIDS due to Blood Transfusion:

The life assured being infected by HIV or Acquired Immunodeficiency

Syndrome but only if: a) The infection is due to blood transfusion received

after the cover start datet b) The infected life assured is not a haemophiliac

c) There is no known cure.

* HIV/AIDS cover for Medical Staff

Infection caused by HIV (Human Immunodeficiency Virus) after the cove

start date of the benefit provided the life assured is a medical staff

and the accident occurred during the course of the life assured's normal

occupational duties and was reported in accordance with the established

occupational procedure for such accidents.Such infection must be considered

by the medical authorities involved to be caused by: a) Needlestick

injury b) Sharp instrument injury c) By exposure to blood d) Blood stained

by body fluid. Infection in any other manner, including infection as

a result of sexual activity or intravenous drug use, is specifically

excluded. Any accident giving rise to a potential claim must be reported

to us within 30 days of the accident taking place. The life assured

must, within 5 days of the accident, have undergone a blood test indicating

the absence of HIV or its antibodies but a further blood test performed

within 6 months of the accident must indicate the presence of HIV or

its antibodies. This benefit will not apply in the event that any medical

cure is found for AIDS or the effects or the HIV virus or a medical

treatment is developed that results in the prevention of the occurrence

of AIDS. We must have open access to all blood samples and be able to

obtain independent testing of such blood samples. Medical staff means

doctors (general practitioners and specialists), nurses, laboratory

technicians, dentists (surgeons and nurses) or ambulance workers. They

must be working in hospitals, specialists medical centres, dental clinics

or polyclinics in Singapore.

21. Motor Neurone Disease

Motor neurone disease of unknown aetiology is characterized

by progressive degeneration of corticospinal tracts and anterior horn

cells or bulbar efferent neurones. These include spinal muscular atrophy,

progressive bulbar palsy, amyotrophic lateral sclerosis and primary

lateral sclerosis.

22. Parkinson's Disease

Slowly progressive degenerative disease of the central

nervous system as a result of loss of pigment containing neurones of

the brain.Unequivocal diagnosis of Parkinson's disease by a consultant

neurologist registered in S'pore where e condition: a) Cannot be controlled

w medication b) Shows signs of progressive impairment c) Renders e life

assured unable to perform 3 or more of the following: bathing, dressing,

using the lavatory, eating, moving in or out of a bed or chair. Only

idiopathic Parkinson's disease is covered. Your policy does not cover

any other forms of Parkinsonism.

23. Chronic Liver Disease

End stage liver disease as evidenced by all of the following:

a) Permanent jaundice b) Ascites c) Encephalopathy. Your policy does

not cover liver disease secondary to alcohol or drug misuse.

24. Lung Disease

End stage lung disease including interstitial lung disease

requiring extensive and permanent oxygen therapy as well as a FEV 1

test result of consistently less than 1 litre.

25. Aplastic Anaemia

Bone marrow failure which results in anaemia, neutropenia

and thrombocytopenia requiring treatment with at least one of the following:

a) Blood product transfusion b) Marrow stimulating agents c) Immuno

suppresive agents d) Bone marrow transplantation

26. Muscular Dystrophy

A hereditary muscular dystrophy confirmed by a neurologist

registered in Singapore resulting in the inability to perform without

assistance 3 or more of the following: bathing, dressing, using the

lavatory, eating, moving in or out of a bed or chair.

27. Bacterial Meningitis

Bacterial meningitis causing inflammation of the membranes

of the brain or spinal cord resulting in permanent neurological deficit.

The diagnosis is to be confirmed by a consultant neurologist.

28. Benign Brain Tumour

A non-cancerous tumour in the brain. Your policy does

not cover cysts, granulomas, malformations in, or of, the arteries or

veins of the brain, haematomas and tumours in the pituitary gland or

spine.

29. Encephalitis

Severe inflammation of brain substance which results in

significant and permanent neurological sequelae as certified by a practitioner

specializing in neurology.

30. Poliomyelitis

Unequivocal diagnosis by a consultant neurologist of infection

by the polio virus leading to paralytic disease as evidenced by impaired

motor function or respiratory weakness. Cases not involving paralysis

and other cases of paralysis are not eligible for this benefit.